Have you ever felt lost trying to choose the right home loan? I know exactly how that feels—I once tried to pick a mortgage and felt confused by all the options. Many people struggle to understand which loan is best for them. If this sounds like your situation, you are not alone.

This guide will solve that problem. Here, we will explain Arvest Mortgage services, different loan types, account management, and refinancing. By the end, you will clearly know how to handle your mortgage confidently and make informed decisions for your home financing.

What Is Arvest Mortgage?

Arvest Mortgage is a home lending service that helps people buy, refinance, and manage residential property loans. They offer a range of options for different financial situations. The company focuses on making mortgages simple and manageable. With online tools, borrowers can monitor their accounts and payments easily.

Mortgage Services Offered

Arvest Mortgage provides conventional loans, government-backed loans, and refinancing options. First-time homebuyers can also access special programs. Their online portal, my.mortgage.arvest.com, allows users to view statements, make payments, and set up automatic payments. Customer support and mortgage servicing help ensure smooth management.

Arvest Mortgage Loan Types

Arvest Mortgage offers several types of loans to meet different needs. Choosing the right one depends on your finances, credit, and home goals.

| Loan Type | Best For | Down Payment | Key Benefit |

|---|---|---|---|

| Conventional Loan | Borrowers with good credit | Usually 3%–20% | Flexible terms, competitive rates |

| FHA Loan | First-time homebuyers | As low as 3.5% | Easier qualification |

| VA Loan | Eligible veterans & service members | Often 0% | No down payment requirement |

| USDA Loan | Rural homebuyers | Often 0% | Affordable financing in eligible areas |

| Jumbo Loan | Higher-priced homes | Varies | Supports larger loan amounts |

Conventional Loans

Conventional loans are standard home loans with fixed or adjustable rates. They are best for borrowers with stable income and good credit. Private mortgage insurance (PMI) may be required if down payment is less than 20%. These loans give flexibility in repayment and terms.

FHA Loans

FHA loans are designed to help borrowers who may not qualify for conventional financing. They often require a lower down payment and may be easier to qualify for. This makes them a popular choice for first-time homebuyers. Borrowers should still review income and credit requirements before applying.

VA Loans

VA loans are available to eligible veterans, active-duty service members, and certain military families. One of the biggest benefits is the potential for no down payment requirement. These loans may also offer competitive interest rates and flexible qualification standards. Eligibility is based on military service requirements.

USDA Loans

USDA loans are intended for eligible buyers purchasing homes in approved rural areas. Many qualified borrowers can obtain financing with little or no down payment. These loans are designed to support homeownership in smaller communities. Income limits and property location requirements usually apply.

Jumbo Loans

Jumbo loans are designed for homes that exceed conventional loan limits. Higher credit scores and larger down payments are often required. They allow borrowers to finance expensive properties. Monthly payments may be higher, so careful planning is important.

Fixed vs Adjustable-Rate Mortgages

Fixed-rate mortgages keep the same interest rate over the loan term. This ensures stable monthly payments. Adjustable-rate mortgages (ARMs) may start with lower rates but can change over time. Borrowers should weigh stability against potential savings.

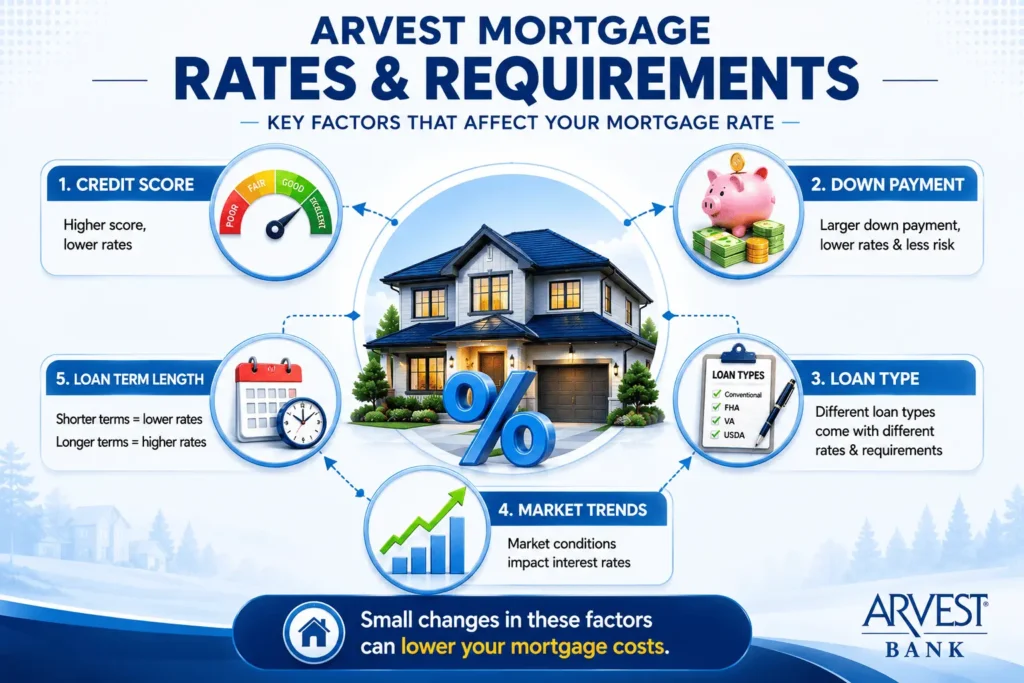

Arvest Mortgage Rates and Requirements

Mortgage rates play a big role in the total cost of a home loan. Even a small difference in interest rate can affect monthly payments over many years. That is why it is important to understand what affects rates before applying. A little research today can save money later.

Current Mortgage Rate Factors

Mortgage rates change based on market conditions, inflation, and lending trends. Your credit score also affects the rate you receive. Borrowers with stronger credit profiles often qualify for better rates. The loan term and down payment amount can also influence the final offer.

For example, two people may apply for the same loan amount. If one has a higher credit score and larger down payment, that person may receive a lower interest rate. Over a 30-year loan, this could lead to significant savings. Small improvements in financial health can make a big difference.

Credit Score Requirements

Credit score is one of the first things lenders review. A higher score shows a history of responsible borrowing. Most conventional loans prefer a score of at least 620, while some government-backed programs may allow lower scores. Improving your score before applying can increase approval chances.

Simple actions can help improve credit health. Paying bills on time is one of the most effective steps. Reducing existing debt can also help. Checking credit reports for errors is another smart move before applying for a mortgage.

Down Payment and Income Requirements

The required down payment depends on the loan program. Some loans allow a low down payment, while others require a larger amount. A higher down payment may reduce monthly costs and lower overall risk. It can also improve loan approval odds.

Lenders also review income and employment history. They want to see stable earnings and the ability to repay the loan. Consistent employment often strengthens an application. Providing accurate documents helps speed up the review process.

How to Apply for an Arvest Mortgage

Applying for a mortgage may seem difficult at first, but the process follows a clear path. Knowing the steps ahead of time can reduce stress and prevent delays. Most borrowers move through prequalification, application review, underwriting, and closing. Each stage has a specific purpose.

Get Prequalified

Prequalification gives an estimate of how much you may be able to borrow. This step reviews basic financial information such as income, debt, and credit standing. It helps buyers understand their budget before searching for a home. Many people use prequalification as a starting point.

Prequalification is useful because it provides direction. Instead of looking at homes outside your budget, you can focus on realistic options. This saves time and reduces disappointment. It also prepares you for the next stage of the process.

Required Documents

Preparing documents early can make the application process smoother. Most lenders request proof of income, tax records, bank statements, and employment information. Identification documents are also required. Having everything ready helps avoid delays.

A complete file allows underwriters to review information faster. Missing paperwork often causes processing issues. Organizing documents in advance is a simple but valuable step. It shows financial readiness and responsibility.

Application, Underwriting and Closing

After submitting the application, the lender reviews all financial details. This stage is called underwriting. The goal is to confirm that the borrower meets loan requirements and can manage repayment. Additional information may sometimes be requested during this process.

Once approved, the loan moves to closing. This is where final documents are signed and legal details are completed. Closing costs are usually paid at this stage. After closing, the home purchase process is officially complete.

My Arvest Mortgage Login and Payment Management

Managing a mortgage should be simple and convenient. Modern online tools allow borrowers to track account activity without unnecessary paperwork. Payment history, statements, and account details can all be reviewed from one place. This helps homeowners stay informed and organized.

Accessing Your Mortgage Account

The online account portal provides access to important loan information. Borrowers can check balances, review statements, and monitor payment activity. This makes account management easier and more transparent. Quick access to information helps avoid confusion.

Many homeowners prefer digital account access because it saves time. Information is available whenever needed. This reduces the need for phone calls and paperwork. Online tools make mortgage management more convenient.

Making Online Payments

Online payments provide a fast and secure way to manage a mortgage. Borrowers can schedule payments from a connected bank account. Automatic payment options are also available for added convenience. These features help reduce the risk of missed due dates.

Regular payment tracking is important. Reviewing payment history can help identify errors or missed transactions. Staying organized improves financial management. Consistent payments also support long-term financial stability.

Escrow, Taxes and Insurance

Many mortgage loans include an escrow account. Part of each monthly payment is set aside for property taxes and homeowners insurance. The lender then pays these bills when they become due. This simplifies financial planning for homeowners.

Escrow accounts help prevent missed tax or insurance payments. They also spread large yearly expenses across monthly payments. This creates more predictable budgeting. Many borrowers find this approach easier to manage.

Financial Hardship Assistance

Unexpected challenges can affect anyone. Job changes, medical expenses, or financial emergencies may create payment difficulties. Contacting the lender early is usually the best approach. Waiting too long can limit available options.

Many lenders offer programs designed to help borrowers during hardship. These solutions may include temporary payment adjustments or other assistance measures. Every situation is different, so communication is important. Seeking help early often leads to better outcomes.

Arvest Mortgage Refinance Options

Refinancing replaces an existing mortgage with a new loan. Homeowners often refinance to lower interest costs, reduce monthly payments, or change loan terms. The decision should be based on personal financial goals and market conditions. Understanding available options helps determine if refinancing makes sense.

Some borrowers choose a rate-and-term refinance. This option focuses on improving loan terms without taking additional cash. Others prefer a cash-out refinance, which allows access to available home equity. Both options have advantages depending on financial needs.

Refinancing can create long-term savings when interest rates are favorable. However, closing costs should always be considered before making a decision. Comparing expected savings with refinancing costs is important. A careful review helps homeowners make informed choices.

Is Arvest Mortgage Worth It?

Choosing a mortgage lender is a major financial decision. The right choice depends on your budget, loan goals, and long-term plans. Some borrowers focus on low rates, while others value customer support and easy account access. Looking at both advantages and limitations can help you decide if this lender fits your needs.

Pros and Cons

Before applying, it helps to compare the strengths and weaknesses side by side.

| Pros | Cons |

|---|---|

| Multiple mortgage programs for different borrower needs | Loan availability may depend on location |

| Online account management tools | Qualification requirements vary by loan type |

| Refinance options available | Interest rates change with market conditions |

| Payment and servicing support | Some programs may require stronger credit profiles |

| Mortgage assistance resources | Not every loan fits every borrower |

The best mortgage is the one that matches your financial situation. A loan that works well for one borrower may not be ideal for another. Reviewing loan terms carefully is always important. Taking time to compare options can lead to a better long-term outcome.

How It Compares to Other Mortgage Lenders

Many lenders offer similar home financing products. The real difference often comes from customer experience, loan flexibility, account tools, and servicing support. Some borrowers compare providers such as Valon Mortgage when researching different mortgage solutions. Comparing rates, fees, and support services can provide a clearer picture.

One borrower may value digital account management, while another may focus on loan variety. Some lenders specialize in first-time buyers, while others focus on refinancing. Understanding personal priorities helps narrow the options. A side-by-side comparison is often the best way to make a confident decision.

Conclusion

At the beginning of this guide, we talked about how confusing the mortgage process can feel. We also promised to make things easier to understand, and hopefully that goal has been achieved. From loan options and eligibility requirements to refinancing and account management, this guide covered the most important details related to Arvest Mortgage. With the right information, careful planning, and a clear understanding of your financial goals, you can move forward with greater confidence and choose a mortgage solution that works for your future.

Frequently Asked Questions

What is the difference between mortgage prequalification and preapproval?

Prequalification is an early estimate of borrowing power based on basic financial information. Preapproval is a more detailed review that includes document verification. Preapproval usually carries more weight when making an offer on a home. Both steps can help buyers prepare for the mortgage process.

Can a mortgage application be denied after prequalification?

Yes, prequalification does not guarantee approval. The lender still reviews income, credit history, debt levels, and supporting documents. Changes in financial circumstances can also affect approval decisions. Providing accurate information is important throughout the process.

How much should I save before applying for a mortgage?

The amount depends on the loan program and personal goals. Buyers should prepare for the down payment, closing costs, and emergency savings. Having extra funds available can provide financial security after moving into a home. Careful planning reduces financial stress.

What is mortgage servicing?

Mortgage servicing refers to the ongoing management of a home loan after closing. This includes collecting payments, managing escrow accounts, and handling customer support. Good servicing helps borrowers stay informed about their loans. It is an important part of the overall mortgage experience.

Can refinancing lower monthly mortgage payments?

In many cases, yes. A lower interest rate or longer loan term may reduce monthly payments. However, refinancing costs should also be considered. Reviewing the total financial impact is important before making a decision.

What happens if I miss a mortgage payment?

Missing a payment may result in late fees and could affect your credit profile. The best approach is to contact the lender immediately if financial difficulties arise. Early communication may help identify available solutions. Taking action quickly can prevent larger problems later.