Your home is your biggest investment, and one missed insurance detail can put it at risk. Many borrowers feel unsure about what arvest mortgage insurance really means, why it shows up on their monthly bill, and who it actually protects. The term gets mixed up with home coverage, escrow charges, premiums, and claim rules all at once. That confusion is normal, and you are not the only one staring at a statement with these questions.

This guide clears up every part of it in plain words. You will learn how arvest mortgage insurance works, what you pay, and how to remove it when the time is right. We will also cover claims, policy rules, the lienholder listing, and how your escrow account handles each premium. By the end, you will know exactly what to do and who to call.

What Arvest Mortgage Insurance Actually Covers

The phrase covers more than one thing, and that is where most people get stuck. When lenders and borrowers talk about arvest mortgage insurance, they may mean private mortgage insurance, the hazard coverage on your home, or the way premiums move through escrow. Each one protects a different party and starts at a different time. If you are new to the lender, our full Arvest Mortgage guide gives you the big picture first.

The reason for the mix-up is simple. All of these items can appear on the same monthly statement and on your yearly escrow analysis. Reading them as one cost makes the bill feel confusing. The table below breaks down the main types so you can see them side by side.

| Type | What it covers | Who it protects | When it applies |

|---|---|---|---|

| Private Mortgage Insurance (PMI) | Lender loss if you default | The lender | Conventional loans with less than 20% down |

| Homeowners / Hazard Insurance | Damage to the home and property | You and the lender | Required for the life of the loan |

| Flood Insurance | Flood damage not covered by a home policy | You and the lender | Homes in high-risk flood zones |

| Lender-Placed Insurance | Basic structure only, at a higher cost | The lender | When your own policy lapses |

One quick note. This is not mortgage protection life insurance, which is a separate policy that pays off your loan balance if you pass away.

Private Mortgage Insurance (PMI) on Arvest Loans

Private mortgage insurance is the type most buyers ask about first. You pay for it each month, but it protects the lender, not you. It applies to conventional Arvest home loans when your down payment is under 20 percent of the price. It can also show up on a refinance when you hold less than 20 percent equity in the home.

The logic behind it is risk. A smaller down payment means the lender takes on more risk, so the policy covers that gap. Once you build enough equity, you can work to drop it. In my years helping buyers, I have found that most people pay PMI for only the first five to seven years of their loan.

How Much Arvest PMI Costs

PMI cost is not the same for everyone. Your rate depends on your loan type, your credit score, and your debt compared to your income. Most borrowers pay between 0.3 and 1.5 percent of the loan each year. On a 200,000 dollar loan, that can mean roughly 600 to 3,000 dollars a year, or about 50 to 250 dollars a month.

A strong credit score and a larger down payment usually mean a lower premium. You can estimate your monthly figure with an Arvest mortgage calculator before you apply. Because your premium also rides on your loan terms, checking current Arvest mortgage rates helps you plan ahead.

FHA Mortgage Insurance Premium (Upfront + Monthly)

FHA loans work a little differently. They use a mortgage insurance premium, or MIP, instead of PMI. You pay an upfront fee of 1.75 percent of the loan at closing, which can be rolled into the balance. On top of that, you pay a monthly amount as part of your payment.

There is one key catch with FHA loans. If your down payment is under 10 percent, the MIP usually stays for the life of the loan. With 10 percent or more down, it can fall off after 11 years. Many borrowers refinance into a conventional loan later just to escape this lifelong cost.

Why VA and USDA Arvest Loans Skip PMI

Not every loan carries this cost. VA loans for veterans and active service members do not require monthly mortgage insurance at all. They use a one-time funding fee instead, which can also be financed. USDA loans for rural buyers work the same way, with a small upfront fee and a low annual fee built in.

If you qualify for either one, you can avoid PMI while still putting little money down. This is one of the biggest savings most eligible buyers overlook. It is always worth asking your loan officer if you fit the rules. The difference can add up to thousands over the years.

How to Remove PMI From Your Arvest Mortgage

The good news is that PMI does not last forever on a conventional loan. Federal law gives you clear ways to cancel it once you owe less on your home. These rules come from the Homeowners Protection Act of 1998. Below are the main paths to drop it.

Automatic PMI Termination at 78% LTV

Your servicer must drop PMI on its own once your loan balance hits 78 percent of the home’s original value. This point is set by your amortization schedule, not by today’s market price. Your payments must be current for it to happen. You do not need to send a request for this step.

There is also a backup rule called final termination. If you reach the halfway point of your loan term, the PMI must stop even if your balance is still above 78 percent. For a 30 year loan, that midpoint falls at 15 years. This protects owners whose balance drops slowly.

Requesting Cancellation at 80% LTV

You do not have to wait for the automatic point. You can ask in writing once your balance reaches 80 percent of the original value. Extra payments toward your principal can help you reach this mark sooner. Your request must include your loan number and the signatures of all borrowers.

Your servicer will check a few things before they agree. You need a good payment history with no recent late payments. There must be no second lien on the home. In some cases, they may ask for a new appraisal to confirm the value has not dropped.

Removing PMI Through Refinance or New Appraisal

Rising home values can also help you drop PMI early. A new appraisal may show that you now hold enough equity from market growth or home upgrades. Some owners choose to refinance into a new loan with no insurance at all. You can review your choices through an Arvest mortgage refinance before you decide.

Refinancing is not free, so the math has to make sense. Weigh the closing costs of the new loan against the premium you would save each month. If the savings beat the costs within a year or two, it is often worth it. A simple break-even check keeps this decision clear.

How to Confirm Who Owns Your Loan

Your removal rules can change based on who owns your loan. The servicer collects your payment, but an investor like Fannie Mae or Freddie Mac may own the actual debt. You can use their free online lookup tools to check in seconds. Knowing the owner tells you which cancellation steps apply to you.

This step matters more than people think. Each investor sets its own rules on top of the federal law. A quick check up front saves you from a denied request later. It also helps you gather the right papers the first time.

Homeowners and Flood Insurance Arvest Requires

Apart from PMI, your lender requires you to keep your home insured. A homeowners policy, also called hazard insurance, must stay active for the whole loan. It covers fire, storms, and other damage to the building, known as dwelling coverage. Your coverage amount usually has to match at least the loan balance or the full cost to rebuild.

Flood damage is a separate matter. Standard home policies do not pay for floods, no matter how bad they are. If your home sits in a high-risk FEMA flood zone, you must carry a flood policy too. Your lender checks this each year and can escrow the flood premium along with your other bills.

Arvest Bank Mortgagee Clause

A mortgagee clause is the line on your homeowners policy that names your lender as the lienholder. It tells your insurer to include the lender on claim checks and renewal notices. Because every insurer routes these papers to one spot, some borrowers call it the central mortgagee clause. Getting this central clause right keeps your policy tied to the correct loan.

The wording protects the lender if your policy ever changes or cancels. Without it, a claim check might not reach the right party, and that can stall a repair. This is a small detail with a big impact. Always confirm it before your first payment.

How to List Arvest as Mortgagee on Your Policy

Ask your insurance agent to list the bank as the mortgagee using the exact name and address your loan papers show. The listing usually includes the words ISAOA and ATIMA, which protect the lender’s interest if your policy changes hands. Double check the spelling and the loan number. A small error here can delay a future claim.

If you switch insurance companies, you must add the same clause to the new policy. Many lapses happen during this exact switch. Send the updated paperwork right away so there is never a gap. One careful step now prevents a costly mix-up later.

How to Send Proof of Insurance to Arvest

Each year your insurer sends a declaration page that proves active coverage. You need to make sure your lender gets a copy before the old policy expires. Many loan servicers confirm coverage through an online portal such as ihaveinsurance, where you upload the page in a minute. You can also email or mail it to the insurance department listed on your statement.

Set a yearly reminder so this never slips your mind. A missed proof is the top reason owners get charged for coverage they did not want. The upload itself takes only a moment. That small habit saves you stress and money.

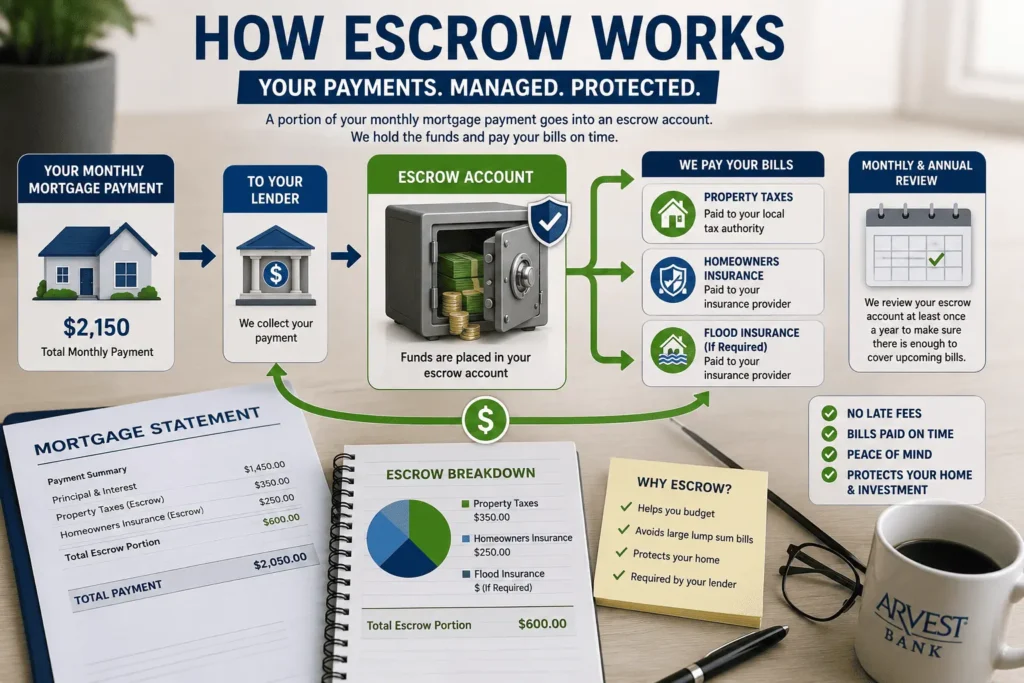

How Escrow Handles Your Insurance Premiums

Part of your monthly payment goes into an account called escrow. This account holds money for your property taxes and insurance premiums. When a bill comes due, your lender pays it for you from the account. Your escrow setup is a big part of how arvest mortgage insurance shows up on your monthly bill.

At least once a year, your lender runs an escrow analysis to check the balance. If taxes or premiums rise, the account can fall short. When that happens, your monthly payment goes up and the shortage is usually spread over the next 12 months. You can track each line and make an Arvest mortgage payment through your online dashboard, or reset access on the Arvest mortgage login page.

Filing an Insurance Claim With Arvest Mortgage

If a storm or fire damages your home, your insurer will send a claim check. Because your lender holds a lien, that check often lists both you and the lender as payees. You cannot simply cash it on your own. You must work with your lender to release the funds for repairs.

Documents Required to Process Your Claim Check

To process your check, your lender needs a few items. These usually include:

- The signed claim check with all parties endorsed

- A copy of the full insurance adjuster’s report

- A signed hazard claim affidavit

- Your loan number written on the front of the check

Send these to the team that handles claims so the work can begin without delay.

How to Endorse Your Insurance Claim Check

Endorsing means signing the back of the check. Every party named on the check must sign before the lender can act, including any contractor or attorney listed. If your loan is current and the damage is small, your local branch may endorse it quickly. Call ahead so an approved signer is ready when you arrive.

How Arvest Disburses Your Claim Funds

Once your lender has the check and papers, the money goes into a separate loss draft account. Funds are then released in stages as your repairs pass inspection. The amount you get at each step depends on the state of your loan. A claim handler will reach out if more papers are needed.

Partial Loss vs Total Loss Claims

A partial loss means your home can be repaired, so funds are released for the work in stages. A total loss is different and far more serious. In that case the insurer pays a large sum, and your lender may apply part of it to the remaining loan balance. If you ever face a total loss, you may also want to review your Arvest mortgage payoff request options.

Lender-Placed Insurance When Your Coverage Lapses

What happens if your home policy lapses or you let it expire? Your lender will not leave the home uninsured against risk. It will buy a policy for you, called lender-placed or force-placed insurance. This coverage is costly and only protects the lender, not your belongings inside the home.

The premium then gets added to your monthly payment, often at a much higher rate than your own policy. I have seen homeowners pay hundreds extra just because a renewal slipped by. The fix is simple, since you only need to keep your own policy active and send proof each year. This single step is one of the most overlooked parts of arvest mortgage insurance, and it can save you real money.

How to Contact Arvest’s Mortgage Insurance Department

When you have a question, it helps to reach the right team the first time. The lender handles most policy papers and claim checks through one central department, which keeps your files in a single place. For payment or escrow questions, your monthly statement lists the correct line to call. You can also find every number sorted by topic in this Arvest mortgage phone number guide, or reach out for general help at james@allthings-mortgage.com.

Conclusion

Buying and keeping a home should feel rewarding, not stressful. As promised at the start, you now know how arvest mortgage insurance works, what you pay, and how to drop it when you qualify. You also know how to handle claims, list your lender, and keep your coverage active all year. Use this guide as your map, and reach out to your lender whenever a new question comes up.

Frequently Asked Questions

Does Arvest mortgage insurance protect me or the lender?

In most cases, this coverage protects the lender, not you. Private mortgage insurance pays the lender if you default on the loan. Your own homeowners policy is the one that protects your house and your belongings from damage or loss.

What is Arvest Bank’s mortgagee clause and address?

A mortgagee clause names the bank as the lienholder on your policy. Ask your agent to list it with the exact name, the ISAOA and ATIMA wording, and the mailing address shown on your loan papers. Confirm the loan number too.

Where do I send my Arvest insurance claim check?

Send your endorsed claim check, the adjuster’s report, and a signed hazard affidavit to the claims team listed on your statement. Write your loan number on the front of the check. The funds then go into a holding account before any repairs are paid.

How long does Arvest take to release insurance claim funds?

After your lender receives the check and all papers, the first payment often goes out within one business day. The full amount is released in stages as repairs are inspected. Timing depends on the size of the loss and your current loan status.

Can I cancel PMI on my Arvest mortgage early?

Yes. You can ask in writing once your balance reaches 80 percent of the home’s original value. Extra principal payments or a new appraisal showing higher value can speed this up. Your loan must be current for the request to be approved.