Paying more on your home loan than you should is a frustrating feeling. Maybe your interest rate is higher than what lenders offer today. Or maybe your monthly payment eats up too much of your budget. Many homeowners with Arvest loans face this same problem and wonder if refinancing could fix it.

The good news is that you can solve this with the right information. This guide explains everything about Arvest mortgage refinance in simple words. You will learn the loan options, requirements, costs, steps, and timelines. By the end, you will know exactly if refinancing with Arvest is the right move for you.

What Is Arvest Mortgage Refinancing?

Refinancing means replacing your current home loan with a new one. The new loan can have a lower rate, a different term, or give you cash from your equity. Arvest mortgage services are offered through Arvest Bank, a community bank based in Arkansas.

Arvest has branches in Arkansas, Kansas, Missouri, and Oklahoma. However, it lends in 45 states across the country. The bank does not lend in Delaware, Maryland, New Hampshire, New York, and Rhode Island. Arvest also services about 99% of the loans it creates, so your loan stays with the same team.

This matters because many lenders sell loans after closing. With Arvest, you usually deal with one company from start to finish. The bank has more than 50 years of home lending experience. That history gives borrowers a trusted partner for refinancing.

Arvest Mortgage Refinance Options

Arvest offers three main ways to refinance your home loan. Each option serves a different goal. Pick the one that matches your financial needs.

Rate-and-Term Refinance

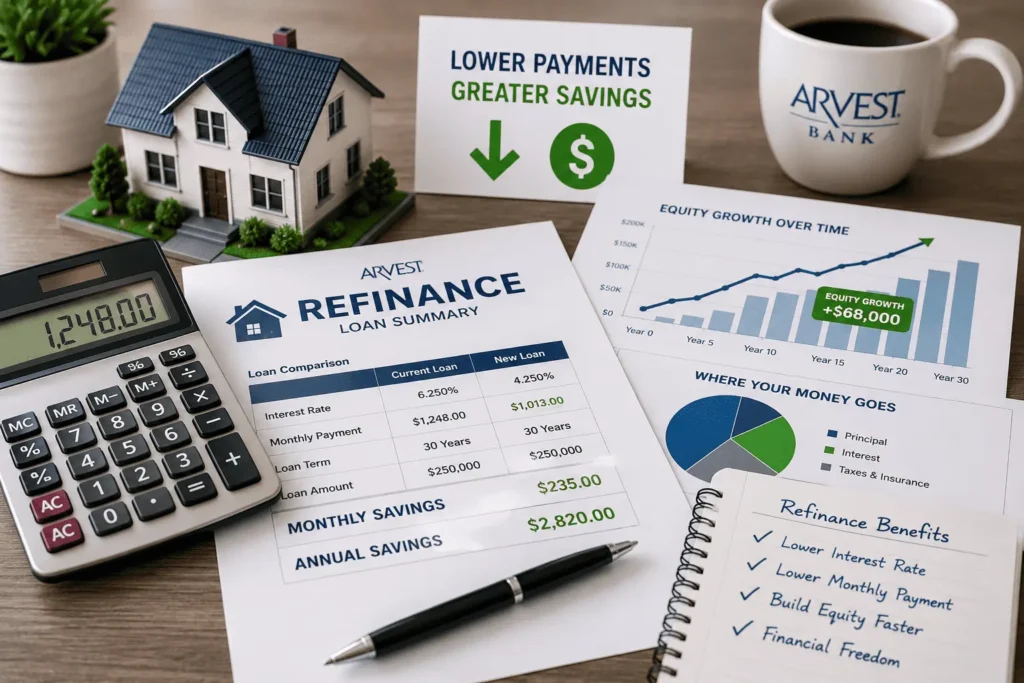

This option changes your interest rate, your loan term, or both. Your loan balance stays almost the same. Homeowners use it to lower their monthly payment when rates drop. Even a 0.50% rate cut can save you thousands over the life of your loan.

Cash-Out Refinance

An Arvest cash out refinance lets you borrow more than you owe. You receive the difference in cash at closing. People use this money for home repairs, debt payoff, or big expenses. Keep in mind that this raises your loan balance and ties more debt to your home.

Shorter Loan Term Refinance

This option moves you from a longer term to a shorter one. For example, you can switch from a 30-year loan to a 15-year loan. Your monthly payment may rise, but you build equity much faster. Cutting 10 years off your term can grow your equity within the first 60 payments.

Which Loans Can You Refinance With Arvest?

Arvest supports refinancing across almost every major mortgage loan program. This wide range helps borrowers with different needs and credit profiles.

Conventional loans: These come in fixed-rate and adjustable-rate options. Fixed rates stay the same for the full term. Adjustable rates start low and change after the initial period.

FHA loans: These government-backed loans work well for borrowers with lower credit scores. They allow easier qualification rules than conventional loans.

VA loans: Veterans and their spouses can refinance with strong benefits. VA refinancing can offer up to 100% financing with no monthly mortgage insurance.

USDA loans: These rural development loans serve homes in qualifying rural areas. They come with low mortgage insurance costs.

Jumbo loans: Homes priced above the conforming limit need jumbo financing. Arvest offers jumbo refinancing in fixed and adjustable forms.

Why Refinance With Arvest Bank?

Arvest gives borrowers some real advantages over many national lenders. These benefits make the process smoother and more personal.

- You get a dedicated loan officer who guides you from application to closing.

- Arvest lets you lock your rate up to 60 days before closing, which protects you from rate jumps.

- The bank services nearly all its own loans, so your servicer rarely changes.

- More than five decades of lending experience backs every refinance decision.

- Real-time phone support is available Monday through Friday during business hours.

These points matter most when rates move fast. A 60-day rate lock is longer than what many lenders offer. That extra time gives you peace of mind while your paperwork moves forward.

Arvest Mortgage Refinance Rates Today

Arvest does not publish refinance rates on its website. The posted rates apply to purchase loans only. To get your exact refinance rate, you must speak with a loan officer.

Your rate depends on several personal factors. These include your credit score, loan amount, loan type, and loan-to-value ratio. Your location also plays a role since rates vary by state. Rates change daily, so you should sign a rate-lock agreement to protect your quote.

If you want a full breakdown of current numbers, check our guide on Arvest mortgage rates. Comparing your current rate with today’s rates is the first step. A meaningful gap between the two often signals a smart time to refinance.

Arvest Refinance Requirements

You must qualify for the new loan just like your original mortgage. Arvest reviews your income, credit, and home equity during underwriting. The table below shows the common standards borrowers should expect.

| Requirement | Typical Standard |

|---|---|

| Credit score (conventional) | Around 620 or higher |

| Credit score (FHA/VA) | Often lower, near 580 |

| Debt-to-income ratio | Generally no more than 45% |

| Home equity | More equity means better terms |

| Income proof | Stable and documented income |

Your debt-to-income ratio is a key number here. It compares your monthly debts to your monthly income. Arvest generally caps this ratio at 45%, though it depends on your credit and loan details. Stronger credit scores unlock better rates and more flexible terms.

How to Refinance Your Mortgage With Arvest

The refinance process follows clear steps from start to finish. Here is how it works:

- Set your goal. Decide if you want a lower rate, a shorter term, or cash out.

- Prequalify online. Use the Arvest Home4Me app or the website to start your inquiry.

- Connect with a loan officer. A specialist contacts you to discuss your options and numbers.

- Submit your documents. Provide income proof, bank statements, and your current loan details.

- Complete the appraisal. Arvest orders an appraisal to confirm your home’s current value.

- Lock your rate. Sign the rate-lock agreement to secure your quoted rate.

- Close the loan. Review the Closing Disclosure, sign the papers, and your new loan begins.

After closing, you can manage your new loan online. The Arvest mortgage login portal lets you track payments, view statements, and check your escrow account anytime.

Documents Needed for an Arvest Refinance

Having your papers ready speeds up approval. Gather these items before you apply:

- Recent pay stubs covering the last 30 days

- W-2 forms and tax returns from the past two years

- Bank statements from the last two to three months

- Your current mortgage statement showing the balance

- Homeowners insurance policy details

- Investment or retirement account statements if needed

Self-employed borrowers may need extra paperwork. This often includes profit and loss statements or business tax returns. Your loan officer will tell you exactly what applies to your case.

Arvest Refinance Closing Costs and Fees

Refinancing is not free, and you should plan for closing costs. These costs typically run between 2% and 5% of your loan amount. On a $200,000 refinance, that means $4,000 to $10,000.

Common fees include the appraisal fee, credit report fee, and origination fee. Title fees, property taxes, and insurance costs may also apply. Arvest notes that additional fees can apply to refinance transactions compared to purchase loans.

The law protects you here in two ways. Arvest must send you a Loan Estimate after you apply. You also receive a Closing Disclosure at least three days before closing. Both forms list every fee, so review them carefully before signing.

When Does Refinancing With Arvest Make Sense?

Refinancing makes sense when your savings beat your costs. The simple way to check this is the break-even point. Divide your total closing costs by your monthly savings. The answer tells you how many months it takes to recover your costs.

Here is an example with easy numbers. Say your closing costs are $5,000 and you save $200 per month. Your break-even point is 25 months. If you plan to stay in your home longer than that, refinancing pays off.

You can run your own numbers with the Arvest mortgage calculator before talking to a lender. Refinancing also makes sense when you want to drop mortgage insurance. If your home value grew and you now have 20% equity, a refinance can remove PMI. Lowering your monthly Arvest mortgage payment frees up money for savings or other goals.

Skip refinancing if you plan to move soon. You may sell the home before reaching your break-even point. In that case, the closing costs are money lost.

How Long Does an Arvest Refinance Take?

Most refinances with Arvest take 30 to 45 days from application to closing. The 60-day rate lock fits this timeline with room to spare. Simple rate-and-term refinances usually close faster than cash-out loans.

A few things can slow the process down. Missing documents, appraisal delays, and title issues are the most common causes. You can speed things up by responding to your loan officer quickly. Sending complete documents the first time also saves days of back and forth.

How to Contact Arvest Mortgage for Refinancing

Talking to a real person makes refinancing decisions easier. Arvest’s refinance team is available Monday through Friday from 8:00 a.m. to 7:00 p.m. CST. You can call the dedicated refinance line at (844) 916-2902.

You can also visit a local branch if you live in Arkansas, Kansas, Missouri, or Oklahoma. For other contact options and department lines, see our full Arvest mortgage phone number guide. If you have questions about this article, you can reach us at james@allthings-mortgage.com.

Conclusion

As promised at the start, this guide gave you the complete picture of refinancing your home loan with Arvest. You now know the options, requirements, costs, steps, and the break-even math that shows when refinancing pays off. The smart next move is to compare your current rate with today’s offers and run your numbers. With this knowledge, your Arvest mortgage refinance decision will be a confident one, not a guess.

Frequently Asked Questions

Does Arvest publish refinance rates online?

No, Arvest does not post refinance rates on its website. Published rates apply only to purchase loans. You must contact a loan officer at (844) 916-2902 to get a personal refinance rate quote based on your credit and loan details.

What credit score do you need to refinance with Arvest?

Most conventional refinances need a credit score around 620 or higher. Government-backed options like FHA loans may accept scores near 580. Higher scores earn better rates, so improving your credit before applying can help lower your monthly payment.

Can I get a cash-out refinance with Arvest?

Yes, Arvest offers cash-out refinancing on qualifying homes. You borrow more than your current loan balance and receive the difference in cash at closing. Borrowers often use these funds for home improvements, debt consolidation, or other large financial needs.

Which states does Arvest offer refinancing in?

Arvest lends in 45 states across the country. It does not lend in Delaware, Maryland, New Hampshire, New York, or Rhode Island. Physical branches are located in Arkansas, Kansas, Missouri, and Oklahoma for borrowers who want in-person service.

Are there fees to refinance with Arvest?

Yes, refinancing comes with closing costs of about 2% to 5% of your loan amount. These include appraisal, origination, and title fees. Arvest provides a Loan Estimate and a Closing Disclosure that list every fee before you sign.

Can I refinance an FHA or VA loan with Arvest?

Yes, Arvest refinances both FHA and VA loans. VA refinancing offers strong benefits, including up to 100% financing and no monthly mortgage insurance. FHA refinancing helps borrowers with lower credit scores qualify more easily than conventional loan options.

How do I start my Arvest refinance application?

Start by prequalifying through the Arvest Home4Me app or the Arvest website. You can also call a loan officer directly to begin. After prequalification, you submit documents, complete an appraisal, lock your rate, and close your new loan.